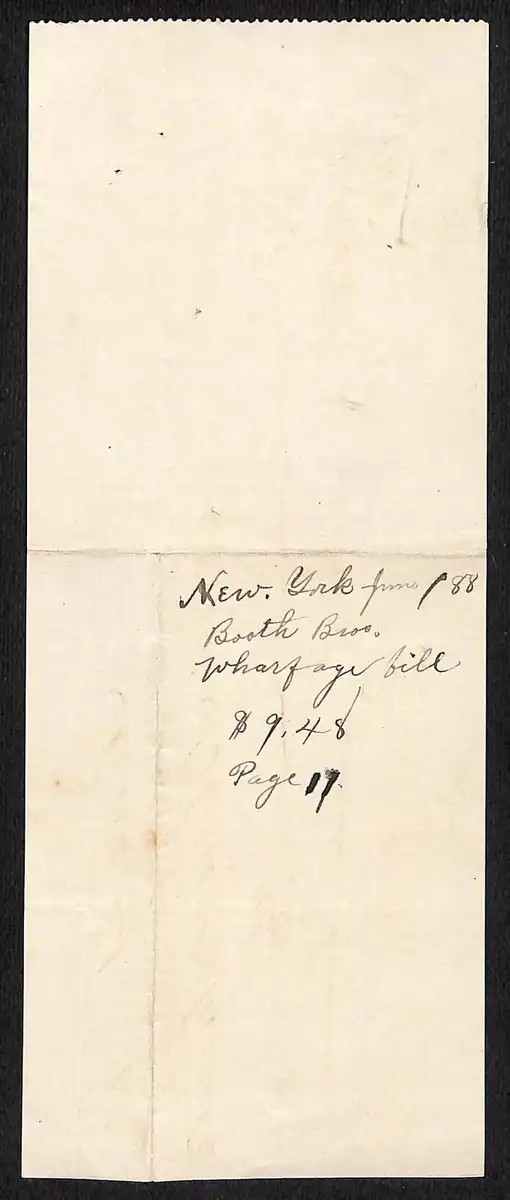

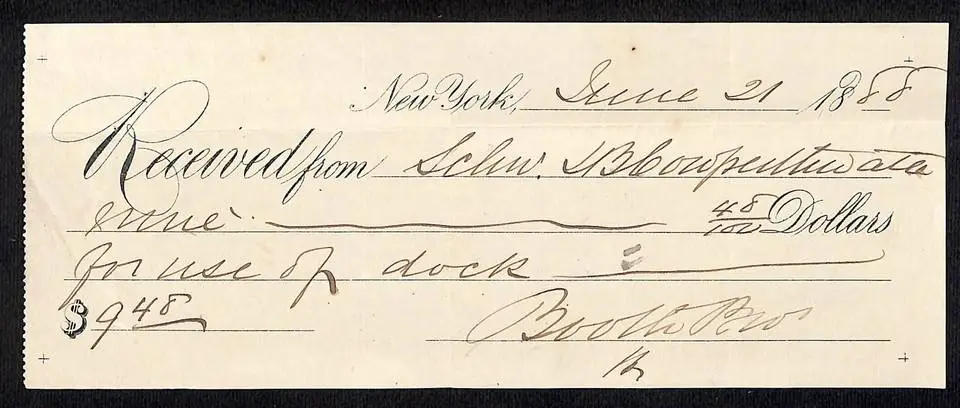

First, my thanks to Bart Rosenberg who alerted me to this lot in this past weekend's auction by Golden Oaks. I had looked at the revenue lots, but completely glossed over this one. There was one other active bidder, and I ended up winning it for considerably less than I thought it might sell for.

Extremely unusual, possible (probable?) uses of postage stamps for fiscal purposes. I don't know whether the uses are improper or illegal, but I'm pretty sure they are not postal.

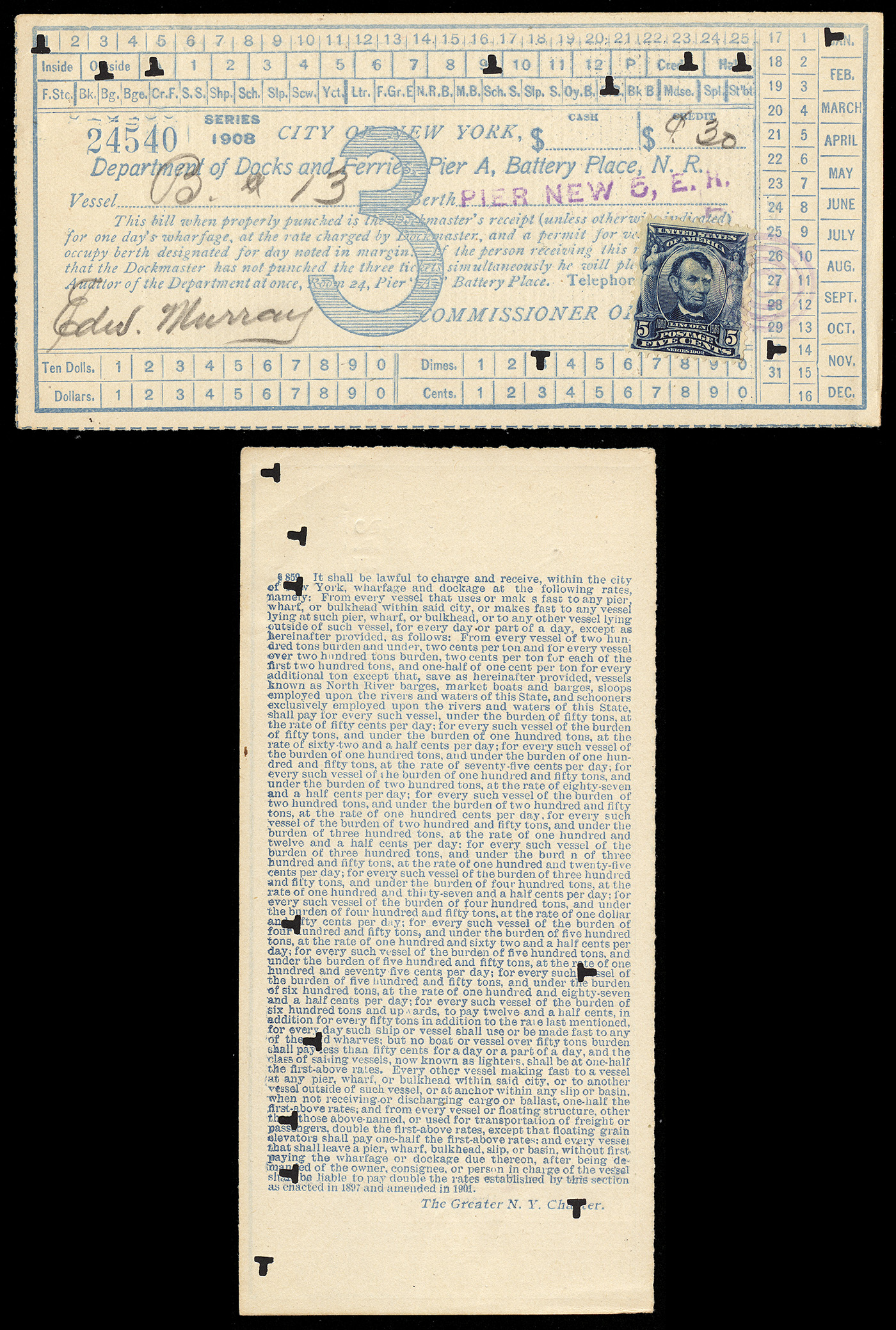

They are two New York City docking fee tickets, one from 1906 and one from 1908, both with postage stamps affixed and tied.

The dates fall outside of the Spanish American War (battleship) federal tax period, so off the top of my head, the possibilities are:

1. A state tax of some sort

2. A local/municipal tax

3. A handling/processing fee

4. None of the above; these are fake/contrived.

What causes me to think it's not #4 is that if so, they did a very good job, as the magenta inks match, and the date of the tying cancel matches the date punched on the front of the card.

Beneath the two images below, I've added what Google Gemini responded to my prompts about them.

Any thoughts or suggestions as to what these are is greatly appreciated.

My initial prompt when uploading the first image (1906):

Quote:

This is both sides of a 1906 docking receipt with a U.S. postage stamp affixed to the back, presumably improperly used as a revenue stamp to pay a state or municipal tax or fee (there were no federal taxes in play at this time). Provide 1. A list of possible taxes or fees that this might have paid, and 2. provide a precise transcription of the text on both front and reverse.

Response:

1. Possible Taxes or Fees PaidQuote:Based on the "Greater N.Y. Charter" text on the reverse and the nature of the "Department of Docks and Ferries," the stamp likely represented one of the following:

- Wharfage/Dockage Fees: The most likely candidate. The reverse side explicitly quotes Section 859 of the Charter regarding rates for vessels making fast to piers. While the bill itself is the receipt, the stamp may have been an attempt to satisfy a local filing fee or a "notary-style" authentication fee for the transaction.

- Harbor Master/Dockmaster Fees: A small administrative fee for the specific assignment of a "berth" or "slip" by the dockmaster, as mentioned in the bill's main text.

- City Revenue/Documentary Fee: New York City occasionally experimented with small fees for official municipal receipts to fund port improvements or maintenance.

- Convenience "Tax": Occasionally, if a clerk lacked official city fee stamps or if a small administrative charge was due, a postage stamp was used as a "placeholder" for value, even though it was technically invalid for non-postal use.

2. Document TranscriptionFront (Main Bill)

Quote:

No. 135802 | SERIES 1906 | CITY OF NEW YORK

Department of Docks and Ferries, Pier A, Battery Place, N. R.

Vessel: [Handwritten: S.S. [unclear] 12] | Berth: [Handwritten: Pier 3 E.R.]

This bill when properly punched is the dockmaster's receipt (unless otherwise indicated), for one day's wharfage, at the rate charged by dockmaster, and a permit for vessel named, to occupy berth designated for day noted in margin.

[Signed] Cash | COMMISSIONER OF DOCKS.

Reverse (The Charter Text)

Quote:

§ 859. It shall be lawful to charge and receive, within the city of New York, wharfage and dockage at the following rates, namely: From every vessel that uses or makes fast to any pier, wharf, or bulkhead within said city, or makes fast to any vessel lying at such pier, wharf, or bulkhead, or to any other vessel lying outside of such vessel, for every day or part of a day except as hereinafter provided, as follows: From every vessel of two hundred tons burden and under, two cents per ton; and for every vessel over two hundred tons burden, two cents per ton for each of the first two hundred tons, and one-half cent per ton for every additional ton; except that all canal boats, provided, vessels known as North River barges, lighters, barges, sloops employed upon the rivers and waters of this State, and schooners exclusively employed upon the rivers and waters of this State, shall pay for every such vessel under the burden of fifty tons, at the rate of fifty cents per day; for every such vessel of the burden of fifty tons, and under the burden of one hundred tons, at the rate of sixty-two and a half cents per day; for every such vessel of the burden of one hundred tons, and under the burden of one hundred and fifty tons, at the rate of seventy-five cents per day; for every such vessel of the burden of one hundred and fifty tons, and under the burden of two hundred tons, at the rate of eighty-seven and a half cents per day; for every such vessel of the burden of two hundred tons, and under the burden of two hundred and fifty tons, at the rate of one dollar per day; for every such vessel of the burden of two hundred and fifty tons, and under the burden of three hundred tons, at the rate of one dollar and twelve and a half cents per day; for every such vessel of the burden of three hundred tons, and under the burden of three hundred and fifty tons, at the rate of one dollar and twenty-five cents per day; for every such vessel of the burden of three hundred and fifty tons, and under the burden of four hundred tons, at the rate of one dollar and thirty-seven and a half cents per day; for every such vessel of the burden of four hundred tons, and under the burden of four hundred and fifty tons, at the rate of one dollar and fifty cents per day; for every such vessel of the burden of four hundred and fifty tons, and under the burden of five hundred tons, at the rate of one dollar and sixty-two and a half cents per day; for every such vessel of the burden of five hundred tons, and under the burden of five hundred and fifty tons, at the rate of one dollar and seventy-five cents per day; for every such vessel of the burden of five hundred and fifty tons, and under the burden of six hundred tons, at the rate of one dollar and eighty-seven and a half cents per day; for every such vessel of the burden of six hundred tons and upwards, to pay twelve and a half cents, in addition for every fifty tons in addition to the rate last mentioned, for every day such ship or vessel shall use or be made fast to any of the said wharves; but no boat or vessel over fifty tons burden shall pay less than fifty cents for a day or a part of a day, and the class of sailing vessels, now known as lighters, shall be at one-half the first above rates. Every other vessel making fast to a vessel at any pier, wharf, or bulkhead within said city, or to another vessel outside of such vessel, or at anchor within any slip or basin, when not receiving or discharging cargo or ballast, one-half the first-above rates; and from every vessel or floating structure, other than those above-named, or used for transportation of freight or passengers, double the first-above rates, except that floating grain elevators shall pay one-half the first-above rates; and every vessel that shall leave a pier, wharf, bulkhead, slip, or basin, without first paying the wharfage or dockage due thereon, after being demanded of the owner, consignee, or person in charge of the vessel shall be liable to pay double the rates established by this section as enacted in 1897 and amended in 1901.

The Greater N. Y. Charter.

I then uploaded the second ticket and asked Gemini to analyze it in light of our prior interaction.

The only thing it pointed out was the lengthier inscription on the front of this 1908 ticket:

Quote:

This bill when properly punched is the Dockmaster's receipt (unless otherwise indicated) for one day's wharfage, at the rate charged by Dockmaster, and a permit for vessel named, to occupy berth designated for day noted in margin. If the person receiving this bill finds that the Dockmaster has not punched the three tickets simultaneously he will please notify the Auditor of the Department at once, Room 24, Pier A, Battery Place. Telephone 2141 Broad.

And this possible reasoning behind the change:

Quote:

The 1908 form adds a specific instruction to the vessel owner: "If the person receiving this bill finds that the Dockmaster has not punched the three tickets simultaneously..." This was a measure to prevent "skimming" by dockmasters, ensuring the city's copy, the vessel's copy, and the ledger copy all matched.